Not feeling your current budget? Build your “Couture Budget System” from these personal budgeting methods, techniques, and strategies.

I don’t know of a scarier, more mental-obstacle-inducing money word than ‘budget’.

It’s been blamed for being a youth stealer, a life-enjoyness vampire, and creating money hangovers so strong that you just throw in the towel altogether.

The thing is, budgets are the exact opposite of all of these things when set up to support your life.

So, we’ve gotta make friends with budgets again.

But not in the one-sided way you experienced budgets before.

We’re going to create more of an employer-employee relationship where you get to call the shots and slash anything that does not serve you.

Essentials of Budgeting – The Budgeting System

Like clothes, you want to try on a few different budget systems before settling into “the one”.

And let me tell you – you’ll know when you find the one for you because you’ll no longer dread making a budget.

Instead, you’ll feel supported and like you can DO this.

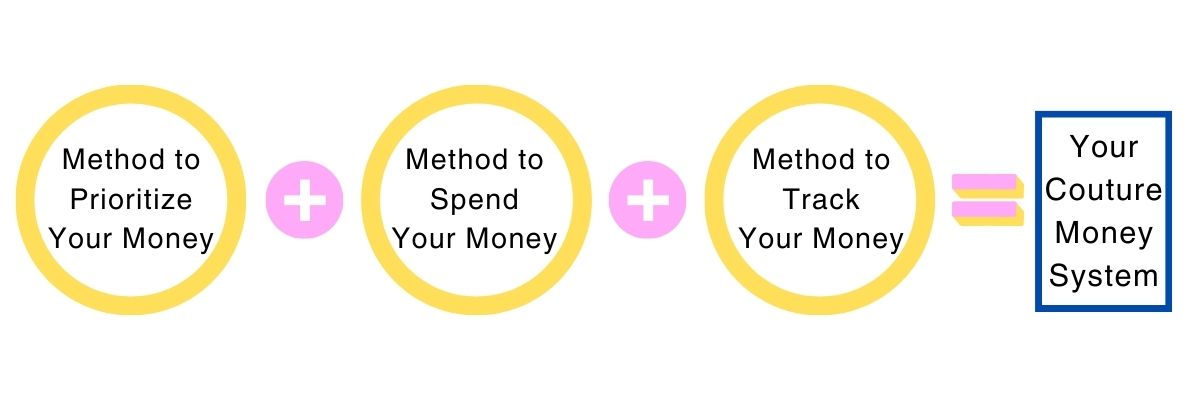

Before we dive into all the different personal budgeting methods out there – so that you can custom-build your Couture Budget System – let me give you an idea about what the heck a budget system is.

A budget system consists of a method to prioritize what to do with your money – spend, save, bill payment, invest, etc. – over a specific period of time, the actual method you choose to spend (or express) those plans, and how you track everything.

For example, my budget system looks like this:

- Method to Prioritize My Money Over a Period of Time: We fill out a household budget worksheet as a guiding “North Star” for several months, and loosely follow the 50%/30%/20%, balanced budget method (50% Necessities/30% Wants/20% Savings and Debt Repayment). Actually, ours looks more like 43% Necessities/13.8% Wants/43.2% Savings (we have zero debt).

- Method to Spend My Money: We use a combination of our debit cards, automated bill payments, manual savings withdrawals, and cash for some “mad money” to spend each week.

- Method to Track My Money: We use a combination of an annual money review, daily receipts, weekly account check-ups, and a monthly glance at our free Empower software.

See how it’s all a system, and not just a cute monthly budget worksheet, or just free printable cash envelopes?

And guess what? Within each of these parts of the system…are various systems to choose from.

Taking Control of Finances with Types of Personal Budgeting Methods

Let me talk about several examples from each moving part.

Methods for Prioritizing Your Money

You can use an Excel budget document, a cute monthly budget worksheet, or something else to physically fill in your budget sheet (aka, how you will prioritize your money over the next period of time – weekly, monthly, etc.).

As far as how to prioritize, well, there are lots of methods for figuring that out.

Choose from these methods to prioritize your money:

- Conscious Spending Plan: Ramit created the Conscious Spending Plan, which has you prioritize your spending into four main categories – fixed costs, investments, savings, and guilt-free spending. The idea is that since you’re conscious about your money and where it’s going, you can stop guilting yourself on whatever you’d like to spend that “guilt-free spending” category on.

- Zero-Based Budgeting: This budget method gives every single dollar (and cent) a “home” in your overall budget plan. In other words, once you fill in your budget plan, you should be left with $0 – there’s no buffer left over in checking for the month (theoretically).

- Balanced Money Formula: You’ve likely seen the 50/30/20 rule, and it’s actually called the balanced money formula (from the book, All Your Worth: The Ultimate Lifetime Money Plan).

- Pay Yourself First (Live on the Rest): This is also called reverse budgeting, and it’s a way for you to prioritize saving your money. You save a percentage of your income, automatically, first (meaning, savings is your top priority), and then you figure out how to live off of the rest.

Methods for Spending According to Your Priorities

How are you going to physically divide up the money you have, and physically spend it, according to the plan you made above?

Choose from these spending methods:

- Cash

- Cash Money Envelopes

- Automated bill pay

- Automated savings account withdrawals

- Direct deposits to savings

- Debit cards

- Credit cards

- Gift Card Spending (where you only upload what you can spend onto gift cards and when the money is out, it’s out)

Methods for Tracking Your Money

Finally, how are you going to track your money (spending, saving, investing, account balances) so that you can figure out if it’s in line with the priorities you set, or not?

Choose from these tracking methods:

- Cash envelopes with spending trackers attached

- Empower (free budgeting software that tracks total net worth, including spending, saving, and investing – it’s what we use)

- Keeping receipts

- Excel budget sheet

- Budget by paycheck worksheets

- Budgeting apps (PearBudget, YNAB, Mint, EveryDollar, etc.)

- Couple’s budget app, and other family budgeting tools

- Spending Tracker Printable (here are free daily spending logs)

- Savings Tracker Printable

- Debt Payoff Tracker Printable

- Bill Payment Tracker Printable

- Sinking Funds free trackers

- YMYL Method: In Your Money or Your Life, the authors outline a method where you track every single little cent that goes into your life (income, inheritances, bonuses, selling items on Facebook, etc.), and that goes out of your life. Then, you compute how many hours you had to work (aka, life energy spent) for what you spend for the month. You create a large wall map, and each month plot your total income and total expenses to ensure you’re spending your life energy the way you want to be. It’s eye-opening!

You can quickly see why I call this the “Couture Budget System” – you can literally choose something from Category A, something from Category B, and something from Category C…and your budget system will look completely different from the next person’s.

It will be tailored to you!

Budget Plan Samples Using These Personal Budgeting Methods

Let’s look at a mish-mash of budget plan samples (what I’m calling Couture Budget Systems) using some of the personal budgeting methods from above.

Couture Budget System Example #1: Tiffany’s Debt-Repayment-Oriented Budget

Stats: Tiffany and her husband make $72,000/year. They have 2 kids (5 and 8 years old), and each work outside of the home. Without the mortgage, these two have $53,000 in debt (student loans and a credit card), and they’re in debt repayment mode.

Tiffany’s household budget system can best be summarized like this:

Method for Prioritizing Money:

- Budget Worksheet: They use a printable budget worksheet to work things out, budget-wise, each month.

Method for Spending According to those Priorities:

- Cash Envelopes for Specific Categories: Tiffany and her husband both get $50/month that they can spend on whatever they would like. Tiffany keeps hers tucked in an envelope marked “Mad Money”, and keeps that in her wallet.

- Bill Auto Pay: They have auto-pay set up for almost all of their bills.

- Debit Cards: Tiffany likes how her spending gets tracked automatically by using a debit card whenever she can. Not only that, but she gets 1% cash back on things like groceries. When they get that bonus, they put it towards their debt repayment.

Method for Tracking Money:

- Couple’s Budget App: They need to stay laser-focused on their money, as they’re in gazelle debt repayment mode. To keep them on the same page with finances, they signed up for a free budgeting app for couples.

- Keep Receipts: Tiffany likes to keep receipts, not necessarily to record everything down, but because she scans them into her Ibotta app to get cash back.

- Debt Tracker printable: What these two really love to track is their progress on each of their debt repayments. They keep a printable debt tracker for each.

Couture Budget System Example #2: Goal-Focused Budgeting

Stats: Rob and his wife, Karen, love to focus on savings goals with their money. Karen stays home with their three children (all under 10), and Rob earns $56,000/year. These two have zero debt.

Rob and Karen’s Couture Budget System can be summarized as follows:

Method for Prioritizing Money:

- Balanced Money Formula: Instead of using the 50% Necessities/30% Wants/20% Savings, they like to break this down into 60% Necessities/15% Wants/15% Retirement and Emergency Fund/10% Savings Goal.

Method for Spending According to those Priorities:

- Gift Card Spending for Wants: They each get to load $75 onto a gift card for the month to whichever store they plan on using it at, and this is their fun money. Once it’s gone, it’s gone! They also have a $40/month gift card just for date nights together. This also helps when they buy a gift for each other – the other person can’t see what was purchased when looking at their bank account!

- Credit Card with Reward Points: These two love racking up reward points, so they have a credit card that they do most of their spending. When the bill comes in each month, they pay it off in the grace period so that they never pay interest (but they earn free airline miles and other goodies!).

- Debit Card for Everything Else: It’s just easier for them to use their debit card if they can’t use their credit card somewhere (doesn’t happen often).

Method for Tracking Money:

- Mint.com: These two use Mint.com (you can now use Empower.com) to track all of their spending (except gift card spending, which they get the same amounts each month). They associated their credit card, and debit cards, and set up spending limits for each category to maintain their balanced money formula. When they’re close to hitting their limits, they receive an alert.

I hope I’ve shown you that there are hundreds of different types of personal budgets and personal budgeting methods. The key is to form your foundation (method to prioritize your money, method to express that priority, and method to track it), and then go from there. Choose your main three elements for your budget system, then tweak it with what you need right now from above to form your own, Couture Budget System.

Amanda L. Grossman is a writer and Certified Financial Education Instructor (CFEI®), Plutus Foundation Grant Recipient, and founder of Frugal Confessions. Over the last 17 years, her money work has helped people with how to save money and how to manage money.

She’s been featured in the Wall Street Journal, Kiplinger, Washington Post, U.S. News & World Report, Business Insider, LifeHacker, Real Simple Magazine, Woman’s World, Woman’s Day, ABC 13 Houston, Keybank, and more. Read more here or on LinkedIn.