Is Credit Sesame a legit site to get my free credit score? Absolutely. Let me show you how to use your free Credit Sesame score to get discounts on your monthly bills.

Do you know how powerful your credit score is? Those three digits have the ability to either increase your monthly payments (if it’s too low), or to really get you some great lending terms that make things like mortgages, homeowner’s insurance, and auto insurance more affordable.

Let me show you just how powerful your credit score can be by harnessing it to actually increase your monthly cash flow.

I’m going to show you how to get your Credit Sesame score for free, as well as 3 ways you can use that information to make phone calls and add money back into your own wallet.

Stick with me – this has the potential to actually open up more cash from your paycheck for you to use however you wish.

What is a Good Credit Score?

This is a bit of a loaded question, because there are several different credit reporting agencies with varying valuation scales, and also because what’s considered a “good credit score” can vary as well.

However, it’s super important to answer because you’re going to be using your credit score to get better financial terms in a few minutes (don’t worry – I’ll show you how).

So, let me give you some pointers as to what you want to shoot for to get your credit score in the “good” range.

First off, there are tons of different credit scores on the market.

Let me just mention a few of the most used ones:

- FICO score – 300 – 850

- VantageScore – 300 – 850

- TransUnion CreditVision – 300 – 850

In general – because each company or lender sets their own ranges for what they consider to be “good” – here are the ranges for what’s considered poor to exceptional:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

What’s the average credit score in the U.S.? According to FICO (meaning, this is the average FICO score), the average U.S. credit score is 717, (up from 706 in 2019), and the average U.S. VantageScore is 701 (up from an average VantageScore of 680 in 2019).

While you almost always have to pay for your credit score (though some credit cards and banking institutions will give you your credit score for free, so you should check with them, also), Credit Sesame actually gives people their credit score for free.

How about that?

Let’s look at what makes Credit Sesame a legitimate place to find out your credit standing.

Is Credit Sesame a Legit Site to Get My Free Credit Score?

Yes, Credit Sesame is a totally legit site where you can get your free credit score.

How do I know this?

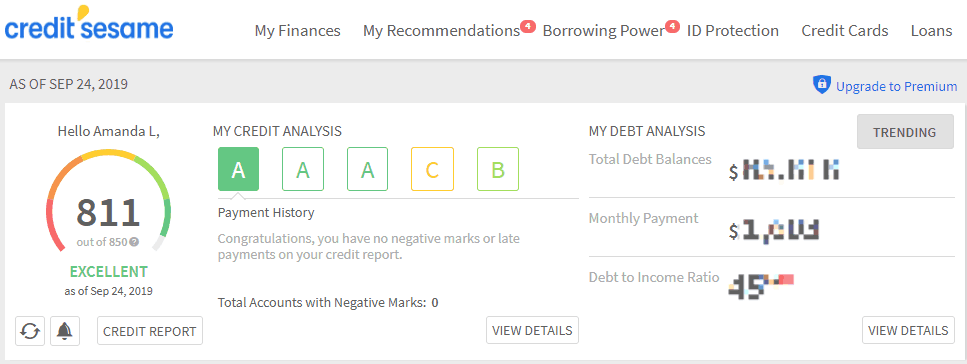

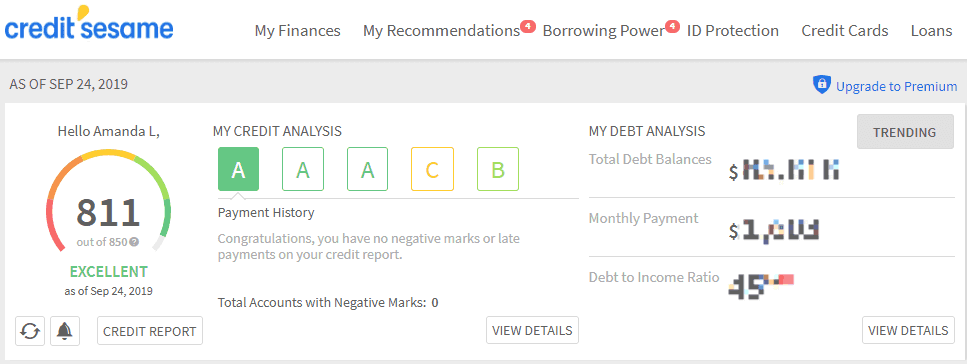

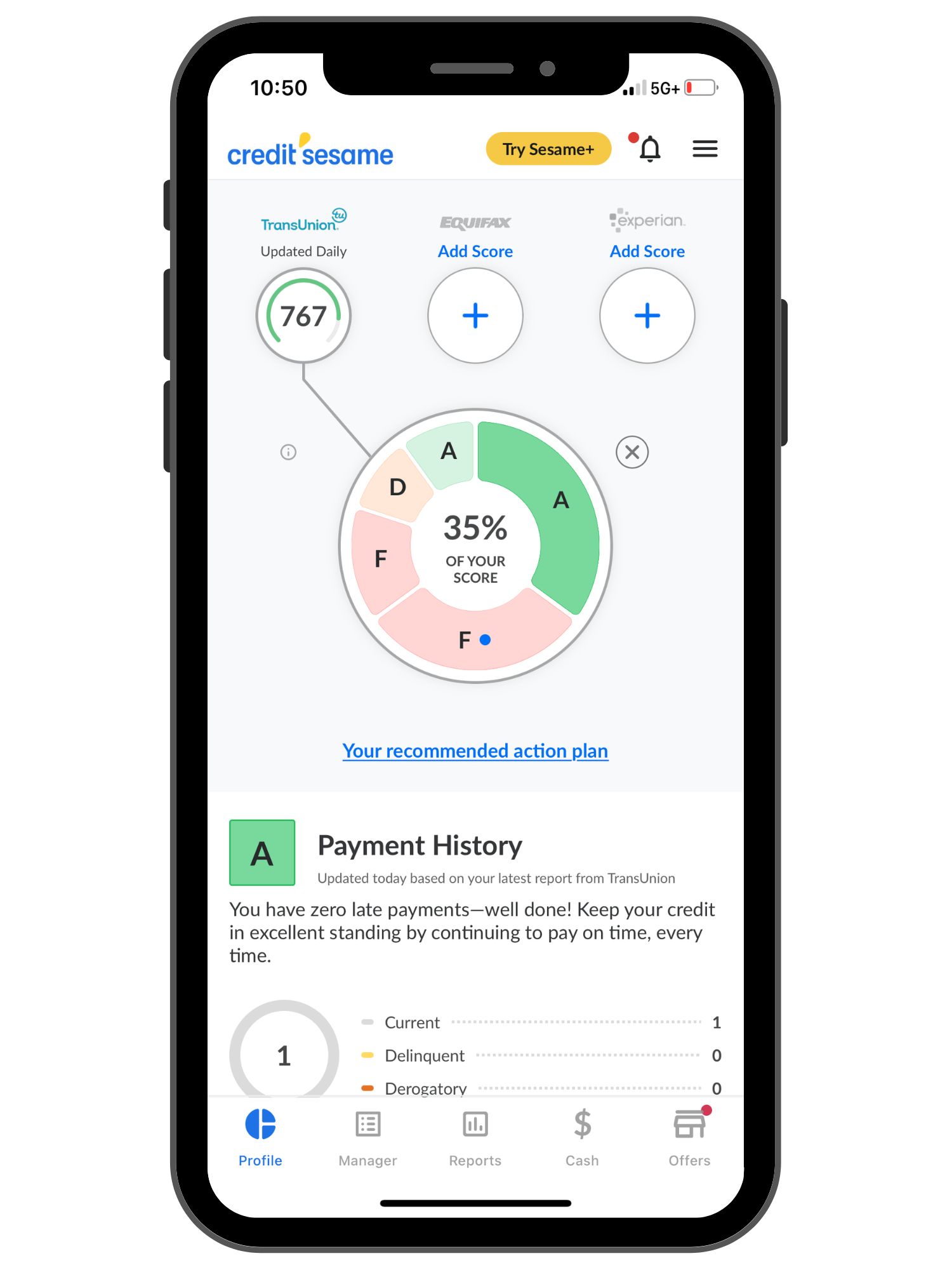

First of all, I use them myself. In fact, I’ll share my own credit score with you below.

Secondly, Credit Sesame has an A+ rating with the BBB (Better Business Bureau). That’s a good sign.

They don’t give you your FICO score – which is used by a majority of lenders – however, you should know that credit scores are just different models working from the same statistics.

What I mean is, if one of your credit scores increases, then it’s likely your other one has increased as well because they use the same information source (your credit report – which you can get for free, annually, through AnnualCreditReport.com), but in varying algorithms (that they keep secret – though we know a bit about what goes into any credit score).

SO, if you can get your hands on any credit score of yours at all, then that’s enough for you to be able to make a dent in your monthly cash flow using the steps I’m going to outline for you below.

What score does Credit Sesame use? They use the VantageScore 3.0, which was developed by the three major credit bureaus, TransUnion, Equifax, and Experian.

Alright…ready to use your credit score to YOUR advantage? Let me show you how.

3 Ways You Can Use Your Free Credit Score Information to Lower Your Monthly Bills

This is where things get fun! Let me walk you through a very actionable strategy for how to use your credit score to lower your monthly bills and/or improve your financial situation.

Step #1: Get Your Free Credit Score

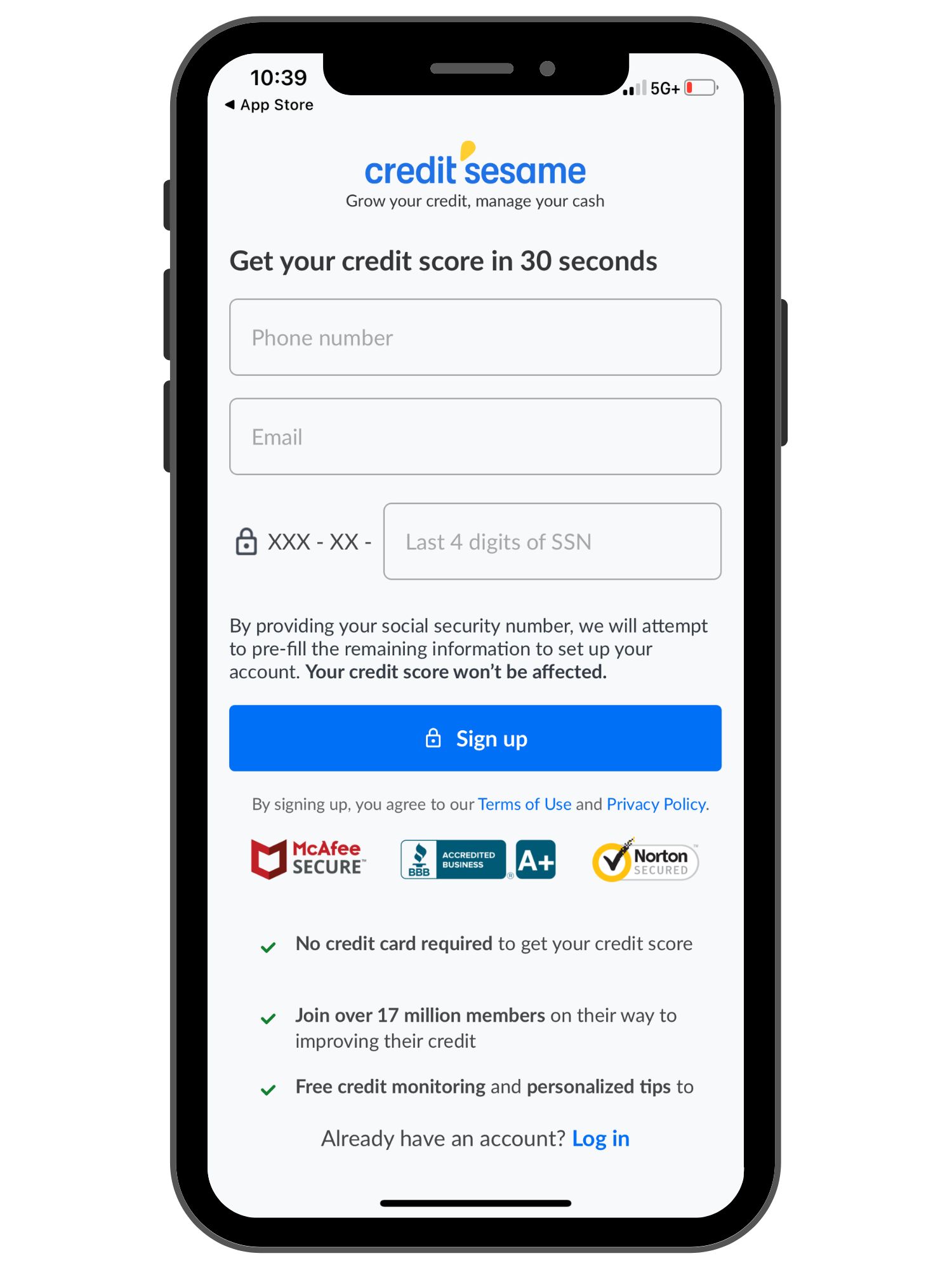

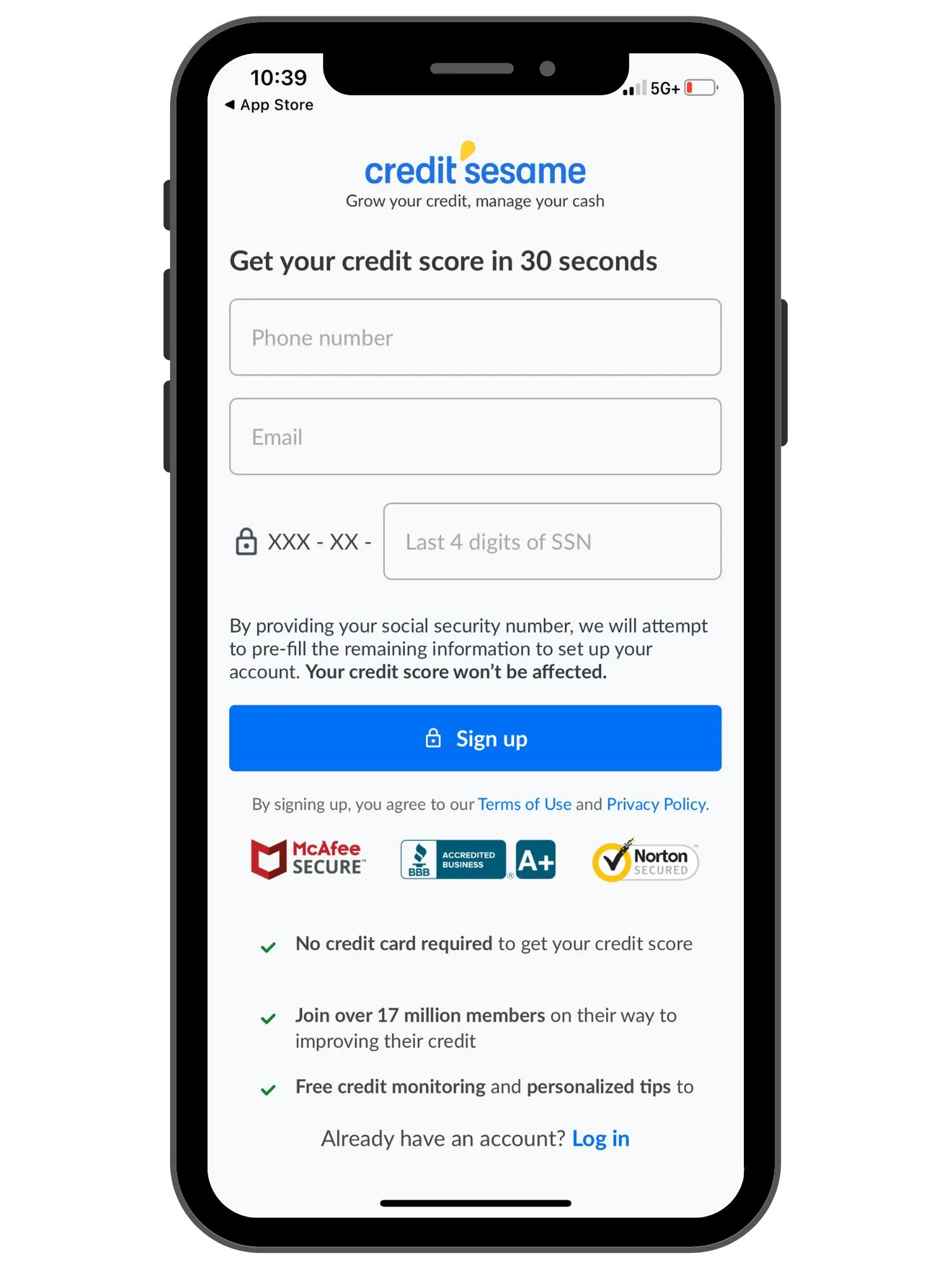

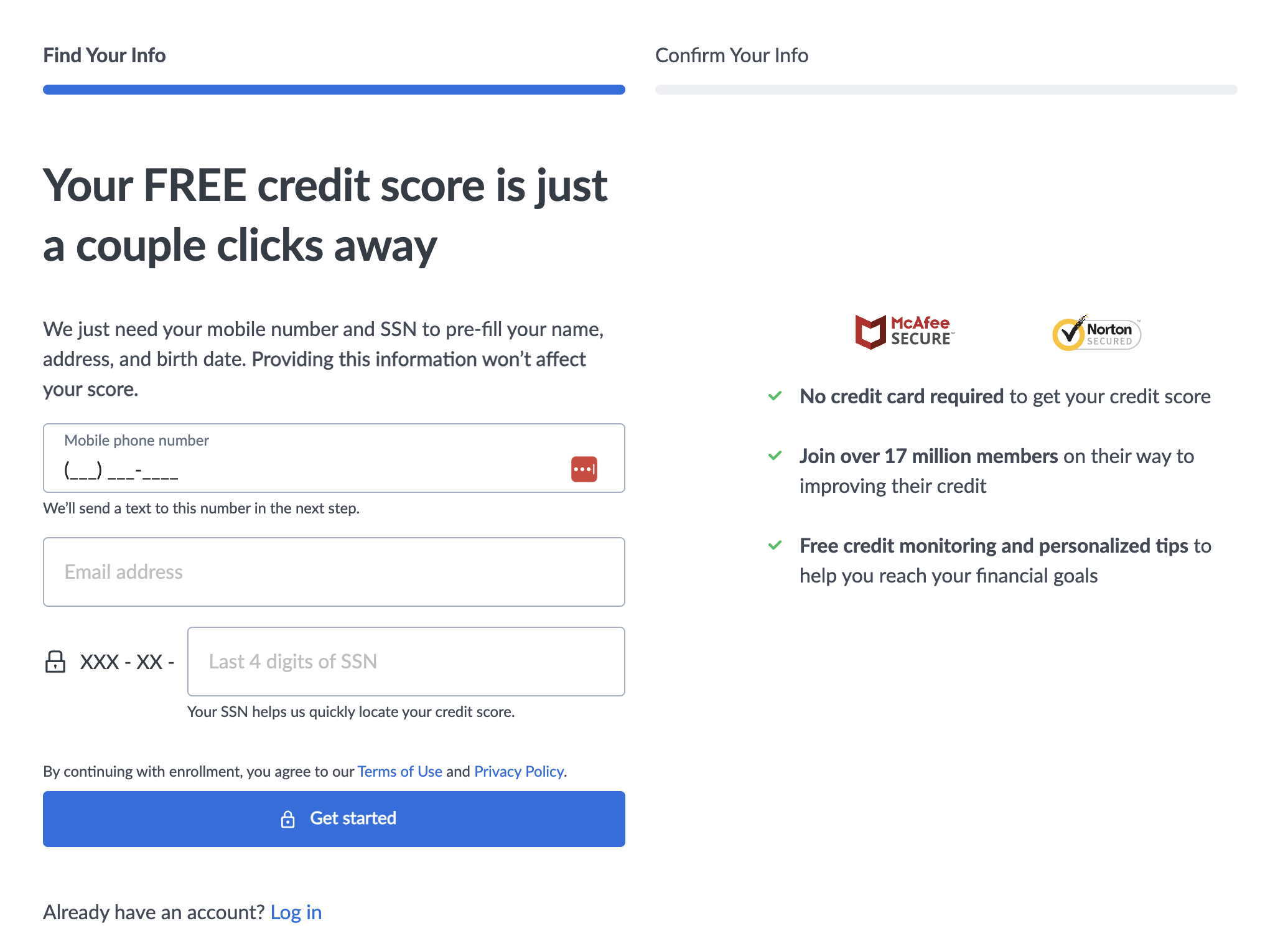

Go to CreditSesame.com to sign up for your free credit score – it’s pretty much an instant process.

Psst: I timed how long it took for me to go from their sign-up screen for a new account all the way to getting my credit score, and it was 1 minute and 57 seconds. Woohoo!

Not only that, but no need to enter your credit card info. How sweet is that? Plus, they now have an app.

Whether you use the app or the desktop version to sign up for a new account, you'll need to put in your email address, mobile phone number, and last four digits of your social security number.

Then, you'll need to confirm or input other information, such as your legal name, your birthday, and where you current live.

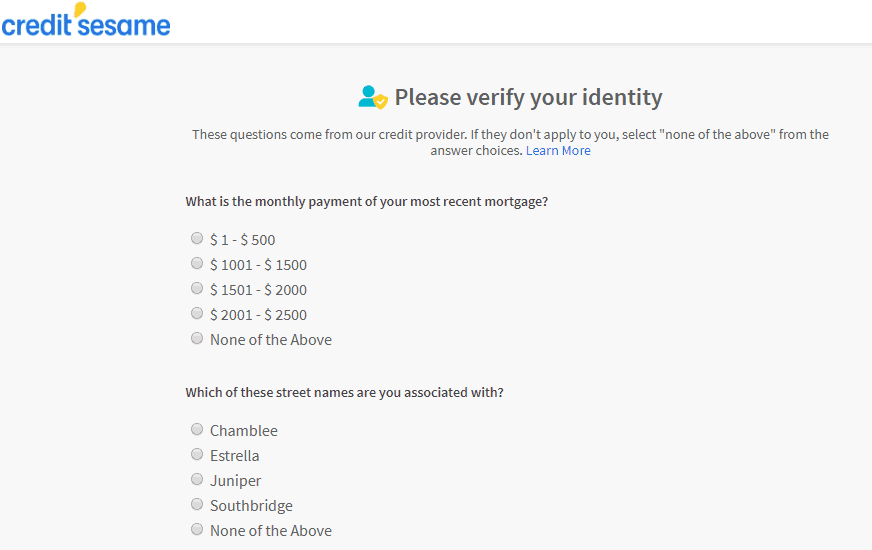

You'll also go through a verification screen, where they gather a few details from your credit report that you'll need to answer.

After you verify…you'll get your score within seconds!

Step #2: Figure Out if It’s Higher than it Used to Be

Alright – so you’re working on improving your credit score, OR, your credit score has already improved since you first signed up for a service or took another financial action.

If you don’t already monitor your credit score, then it might be tricky to figure out if it’s improved or not.

You might still have a hunch that your score has gone up if you’ve been making consistent, on-time payments over the years, or if you’ve paid off a significant amount of debt – like your student loans are paid off or you sold your home.

Credit Sesame automatically updates your credit score every month…so you can check back each month to see how your score is trending (then come back to this article and complete Step #3 when your score has gone up).

Step #3: Choose One of the following 3 phone calls to Make TODAY

Here’s where we make a noticeable improvement to your money. Take just one lunch hour, and call one of the following 3 places to see what kind of discounts you can get.

#1: Your Homeowner’s Insurance Company

The first call you can make is to your homeowner’s insurance. They used your credit score when deciding what your overall insurance rate would be, and so now that you’ve got a better one, ask them to give you a discount.

#2: Your Auto Insurance Company

Did you know that your auto insurance quote is partly based on your credit score? I

f you’ve got a higher one than you previously had when you were first quoted, then it’s definitely time to call and ask them for a new quote. Tell them your credit score has improved, and to please re-quote your account.

#3: Your Credit Card Company

Any debt you rack up on your credit card and don’t pay off at the end of the grace period (typically a month from purchase) is earning interest. It makes sense to use your lower credit score for both:

- Lower Your Interest Rate: Ask for a lower interest rate on your card.

- Get a Balance Transfer: You can potentially open up a new credit card with a 0% balance transfer offer – meaning once you transfer your balance to them, your debt earns 0% interest on it during the introductory period – and pay down your balance sooner.

Let’s move on to a few more things you should know.

How Often Does Credit Sesame Update Your Credit Score?

Now that you have your “baseline” credit score, you’d probably like to know how often your credit score gets updated to reflect a higher score (hopefully – if you’ve been working on improving your credit score).

Especially since you can use that fancy-schmancy higher credit score to then try and negotiate better monthly payments (see below).

Rest assured that your credit score can actually improve in as little as one month, specifically if you work on your payment history and your credit utilization rate when you’re trying to improve it.

A quick recap of what goes into your credit score, and the ways you can improve each category:

- Payment History: What does your payment history say about you? The more consistent, on-time payments you’ve made, the higher your score will be. Improving this part of your score means making sure each month you make your payments on time.

- Credit Utilization: How much credit do you have (your credit line) and how much of that credit are you using? Improving this one could mean paying down your debt so that your credit utilization ratio lowers, and/or getting an increased credit line, which will also naturally lower your credit utilization ratio.

- Credit Age: How old are your credit accounts? Higher scores reflect more aged credit accounts since a creditor can see a longer history of how you’ve been treating your credit.

- Different Types of Credit: There are different types of credit – like a credit card, a mortgage, a car loan, a student loan – and having a variety of credit under your belt is better than just having one variety (in terms of your credit score).

- Amount of Inquiries: A common question about Credit Sesame and any credit score-providing site is “Does Credit Sesame hurt your credit”? The reason people ask this is because certain types of inquiries into your credit score will actually lower your credit score (especially if there are many inquiries at once). Fortunately, Credit Sesame uses a soft-pull inquiry to find out and monitor your credit score. A soft-pull inquiry does not do anything to change your score (versus a hard pull on your credit score, which can lower it). To improve this part of your score, you want to minimize hard pulls on your credit score.

Now, I’m going to show you how to use this information to your advantage, and the 4 simple phone calls you can make to make a real difference to your bottom line (hello, more cash flow!).

FAQs – Frequently Asked Questions

Here’s where I can answer a few more questions you might have (and if you’ve got anymore? Leave them in the comments – I’ll update this article, as needed).

How much does Credit Sesame cost?

Credit Sesame is a free service. In fact, you don’t even need to input any credit card information.

You will not pay anything for the following items

- Your credit score, updated monthly

- Identity protection monitoring

- Debt monitoring

So, how exactly do they make money? They’ll target offers to you that you may or may not want to take advantage of, such as credit cards that you could qualify for or good lending terms for mortgages.

What Credit Agency Does Credit Sesame Use?

Credit Sesame gives you a credit score based on VantageScore, which was developed from the three major credit bureaus: Equifax, Experian, and TransUnion.

Is Credit Sesame a Legit Site?

Yes, Credit Sesame is totally legitimate.

What is a Good Credit Score?

A “Good” credit score is typically between 670 and 739 (according to FICO). However, each lender decides for themselves what they consider to be a “good” credit score. And, remember, the average national score right now is 717 for FICO and 701 for VantageScore.

Amanda L. Grossman is a writer and Certified Financial Education Instructor (CFEI®), Plutus Foundation Grant Recipient, and founder of Frugal Confessions. Over the last 17 years, her money work has helped people with how to save money and how to manage money.

She's been featured in the Wall Street Journal, Kiplinger, Washington Post, U.S. News & World Report, Business Insider, LifeHacker, Real Simple Magazine, Woman's World, Woman's Day, ABC 13 Houston, Keybank, and more. Read more here or on LinkedIn.